MP Market Review – May 10, 2024

Last updated by BM on May 13, 2024

Summary

This is a weekly installment of our MP Market Review series, which provides updates on the financial markets and Canadian dividend growth companies we monitor on ‘The List’.

- Discover how dividend yields guide our stock picks in this week’s newsletter.

- Last week, dividend growth of ‘The List’ stayed the same and has increased by +8.6% YTD (income).

- Last week, price return of ‘The List’ was up with a return of +5.1% YTD (capital).

- Last week, there was one dividend announcement from a company on ‘The List’.

- Last week, there were eight earnings reports from companies on ‘The List’.

- This week, one company on ‘The List’ is due to report earnings.

DGI Clipboard

“Current yield, using its own historic yield as a guide, is, in my view, a fine valuation measure.”

– Tom Connolly

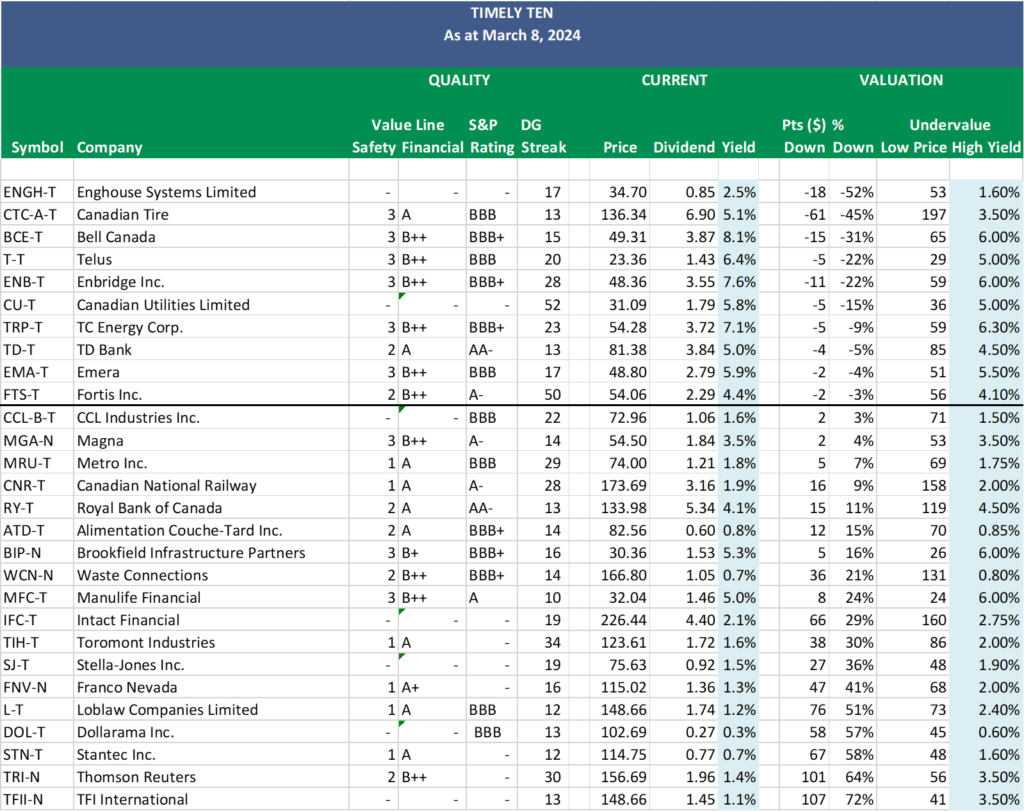

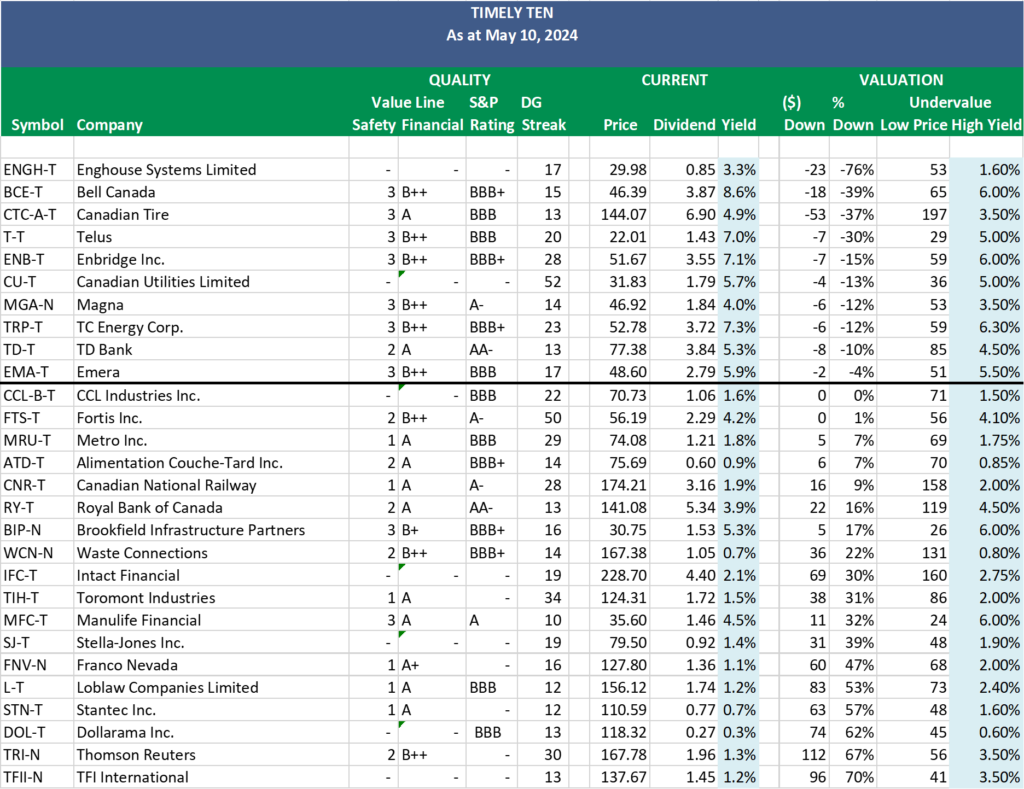

Timely Ten: How Historical Dividend Yields Guide Our Stock Picks

With Q1 2024 earnings behind us now, it’s time to take another look at our ‘Timely Ten’ DGI stocks. These are the ten most undervalued stocks on ‘The List’ according to one of our valuation metrics, dividend yield theory.

Step three in our process involves monitoring our quality dividend growers regularily, which can become quite challenging depending on the number of companies we track. Fortunately, we rely on ‘The List’ instead of the vast array of stocks in the index, which streamlines our task. Nevertheless, we continually seek methods to enhance our efficiency. Through dividend yield theory, we’ve discovered an approach that has proven remarkably effective over the years in aiding us with our efforts.

Dividend yield theory is a simple and intuitive approach to valuing dividend growth stocks. It suggests that the dividend yield of quality dividend growth stocks tends to revert to the mean over time, assuming that the underlying business model remains stable. In practical terms, if a stock pays a dividend yield above its ten-year average annual yield, its price will likely increase to return the yield to its historical average. Knowing that price and yield go in opposite directions, this theory helps us find stocks that are poised for a positive price correction.

We have already pre-screened our candidates using the criteria we laid out in building ‘The List’ initially. This helps us considerably narrow the universe of investable stocks.

- Dividend growth streak: 10 years or more.

- Market cap: Minimum one billion dollars.

- Diversification: Limit of five companies per sector, preferably two per industry.

- Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Next, we rank ‘The List’ by how significantly each stock is priced below its fair value (Low Price), as calculated using dividend yield theory. The stocks that are currently trading below this threshold form our ‘Timely Ten’.

For new investors without a position size in any of the ‘Timely Ten’, your work begins.

Next week, we’ll delve deeper into a couple of stocks from the ‘Timely Ten’ and demonstrate our research process.

DGI Scorecard

The List (2024)

The Magic Pants 2024 list includes 28 Canadian dividend growth stocks. Here are the criteria to be considered a candidate on ‘The List’:

- Dividend growth streak: 10 years or more.

- Market cap: Minimum one billion dollars.

- Diversification: Limit of five companies per sector, preferably two per industry.

- Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

While ‘The List’ is not a standalone portfolio, it functions admirably as an initial guide for those seeking to broaden their investment portfolio and attain superior returns in the Canadian stock market. Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our Canadian dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

For those interested in something more, please upgrade to a paid subscriber; you get the enhanced weekly newsletter, access to premium content, full privileges on the new Substack website magicpants.substack.com and DGI alerts whenever we make stock transactions in our model portfolio.

Performance of ‘The List’

Last week, dividend growth of ‘The List’ stayed the same and has increased by +8.6% YTD (income).

Last week, ‘The List’ ‘s price return was up, with a +5.1% YTD (capital).

Even though prices may fluctuate, the dependable growth in our income does not. Stay the course. You will be happy you did.

Last week’s best performers on ‘The List’ were Stella-Jones Inc. (SJ-T), up +9.67%; Manulife Financial (MFC-T), up +8.34%; and Canadian Tire (CTC-A-T), up +7.51%.

Stantec Inc. (STN-T) was the worst performer last week, down -3.43%.

| SYMBOL | COMPANY | YLD | PRICE | YTD % | DIV | YTD % | STREAK |

|---|---|---|---|---|---|---|---|

| ATD-T | Alimentation Couche-Tard Inc. | 0.9% | $75.69 | -1.4% | $0.70 | 17.4% | 14 |

| BCE-T | Bell Canada | 8.6% | $46.39 | -14.4% | $3.99 | 3.1% | 15 |

| BIP-N | Brookfield Infrastructure Partners | 5.3% | $30.75 | 0.2% | $1.62 | 5.9% | 16 |

| CCL-B-T | CCL Industries Inc. | 1.6% | $70.73 | 22.3% | $1.16 | 9.4% | 22 |

| CNR-T | Canadian National Railway | 1.9% | $174.21 | 4.4% | $3.38 | 7.0% | 28 |

| CTC-A-T | Canadian Tire | 4.9% | $144.07 | 4.0% | $7.00 | 1.4% | 13 |

| CU-T | Canadian Utilities Limited | 5.7% | $31.83 | -0.9% | $1.81 | 0.9% | 52 |

| DOL-T | Dollarama Inc. | 0.3% | $118.32 | 24.5% | $0.35 | 29.5% | 13 |

| EMA-T | Emera | 5.9% | $48.60 | -4.3% | $2.87 | 3.0% | 17 |

| ENB-T | Enbridge Inc. | 7.1% | $51.67 | 6.8% | $3.66 | 3.1% | 28 |

| ENGH-T | Enghouse Systems Limited | 3.3% | $29.98 | -11.7% | $1.00 | 18.3% | 17 |

| FNV-N | Franco Nevada | 1.1% | $127.80 | 16.0% | $1.44 | 5.9% | 16 |

| FTS-T | Fortis Inc. | 4.2% | $56.19 | 2.4% | $2.36 | 3.3% | 50 |

| IFC-T | Intact Financial | 2.1% | $228.70 | 12.5% | $4.84 | 10.0% | 19 |

| L-T | Loblaw Companies Limited | 1.2% | $156.12 | 21.4% | $1.92 | 10.0% | 12 |

| MFC-T | Manulife Financial | 4.5% | $35.60 | 23.3% | $1.60 | 9.6% | 10 |

| MGA-N | Magna | 4.0% | $46.92 | -15.5% | $1.90 | 3.3% | 14 |

| MRU-T | Metro Inc. | 1.8% | $74.08 | 8.1% | $1.34 | 10.7% | 29 |

| RY-T | Royal Bank of Canada | 3.9% | $141.08 | 6.0% | $5.52 | 3.4% | 13 |

| SJ-T | Stella-Jones Inc. | 1.4% | $79.50 | 3.8% | $1.12 | 21.7% | 19 |

| STN-T | Stantec Inc. | 0.7% | $110.59 | 5.7% | $0.83 | 7.8% | 12 |

| T-T | Telus | 7.0% | $22.01 | -7.2% | $1.53 | 7.1% | 20 |

| TD-T | TD Bank | 5.3% | $77.38 | -8.6% | $4.08 | 6.3% | 13 |

| TFII-N | TFI International | 1.2% | $137.67 | 4.9% | $1.60 | 10.3% | 13 |

| TIH-T | Toromont Industries | 1.5% | $124.31 | 10.2% | $1.92 | 11.6% | 34 |

| TRI-N | Thomson Reuters | 1.3% | $167.78 | 17.1% | $2.16 | 10.2% | 30 |

| TRP-T | TC Energy Corp. | 7.3% | $52.78 | 0.9% | $3.84 | 3.2% | 23 |

| WCN-N | Waste Connections | 0.7% | $167.38 | 13.0% | $1.14 | 8.6% | 14 |

| Averages | 3.4% | 5.1% | 8.6% | 21 |

Note: Stocks ending in “-N” declare earnings and dividends in US dollars. To achieve currency consistency between dividends and share price for these stocks, we have shown dividends in US dollars and share price in US dollars (these stocks are listed on a US exchange). The dividends for their Canadian counterparts (-T) would be converted into CDN dollars and would fluctuate with the exchange rate.

Check us out on magicpants.substack.com for more info in this week’s issue….