The 90% Balance Rule

Posted by BM on January 14, 2022

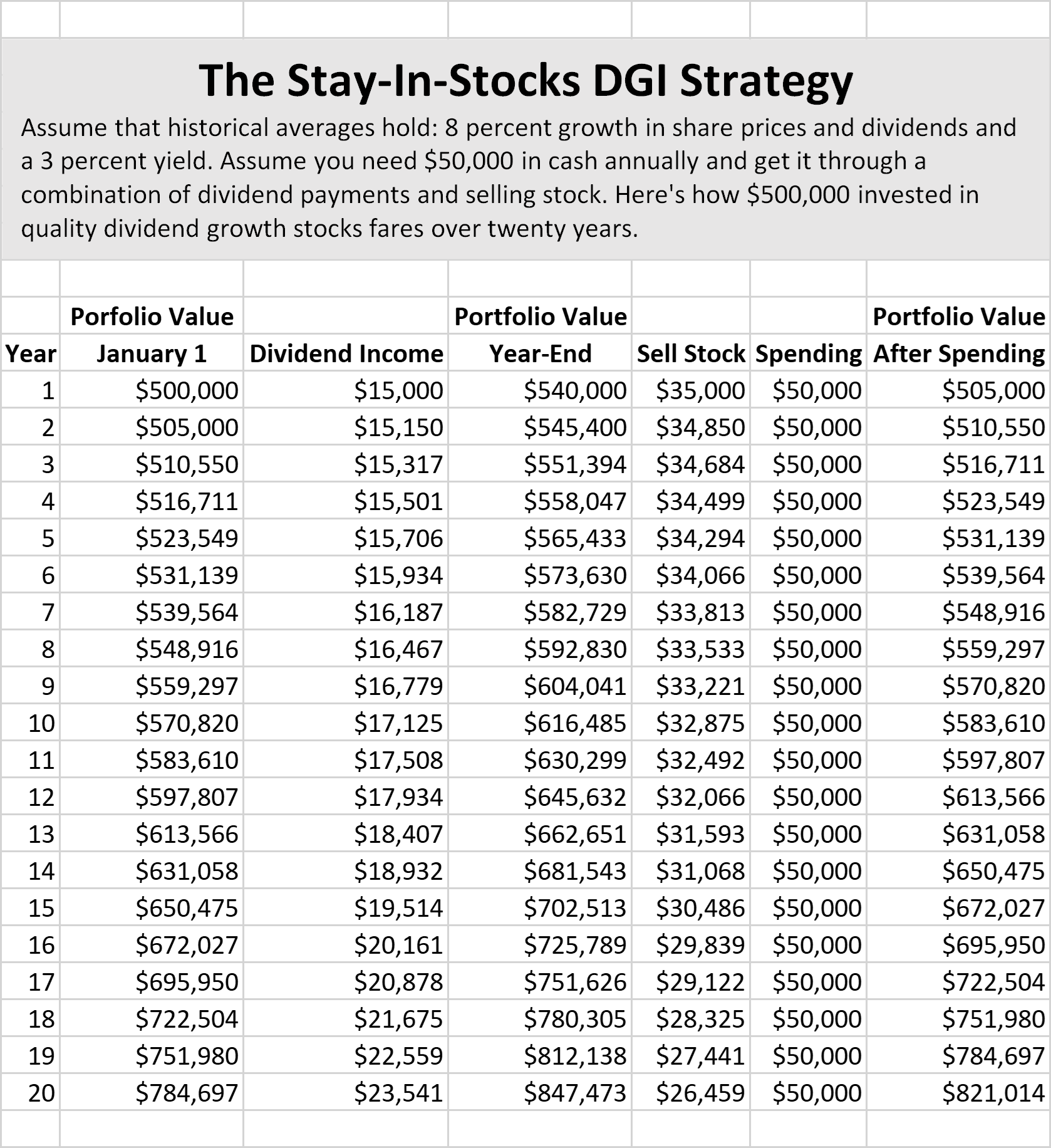

In November last year we wrote a post about Peter Lynch’s Stay-in-Stocks Strategy that he first introduced in 1995. The withdrawal strategy assumes 8% growth in share prices and dividends with a starting dividend yield of 3%. The strategy will generate $50,000 of income each year from a $500,000 portfolio of dividend growth stocks. The average withdrawal rate in this strategy works out to about 8% over the 20 year period.

As a follow up to that article we came across a study titled ‘Income Withdrawal Sustainability using Large Cap Value Portfolio Historical Period 1932 – 2019. An Alternative Strategy for Income Harvesting’.

In the study the author assumes a 7% withdrawal rate using only large cap stocks as part of his portfolio. Some pay dividends and some do not. The concerns voiced in the study are the same as all investors…will we outlive our investments or “spend down” our principal to zero?

Over the period from 1932 – 2019, seventy-one “rolling” twenty-year periods were tested starting at the beginning of the calendar year. Eleven periods, or 15% of total, ended with the portfolio balance falling to zero (failure) at some point along the period.

Lynch’s returns and strategy were based on averages and as we all know, that sometimes can come back and hurt you as it did in this study, 15% of the time.

The most interesting part of the study was the adjustment the author made to improve on the 15% failure rate. The one change is called the ‘90% Balance Rule’.

“If, after the income withdrawal is taken (at the end of each year), the portfolio balance has fallen below “90%” of the original starting amount, then the annual withdrawal taken is reduced by 50%. In subsequent years, the portfolio balance is then monitored for a rise back above the 90% of the original starting amount, at which point a “7%” income withdrawal can be reinstated.

For example, the investor starts with an initial amount of $100K invested in Large Cap value portfolio. At the end of the first year, the portfolio value rises to $110K, so the investor takes a $7K withdrawal. At the end of the second year, with a portfolio loss and $7k income withdrawal the balance falls to $94K, yet still above $90K ( the “90%” of initial starting amount at the beginning of year one ). However, at the end of year three, the portfolio return and income withdrawal reduce the balance to $87K, and therefore, the income withdrawal is reduced to $3500. When the portfolio “gains” and income withdrawal equate to the portfolio values rising back above $90K, then the year’s income withdrawal can be increased “back to” $7K ( 7%).

A compelling feature of this method is that at the end of the year, taking into consideration the portfolio’s “balance level” and year’s return, an investor has a solid grasp as to what dollar amount that their income withdrawal is, and can plan their forward year’s expense budgeting accordingly. They can spread their withdrawal out over the course of the year in equal parts (quarterly for example) or take a larger portion of the withdrawal earlier or later, if emergency needs arise.”

By incorporating the 90% Balance Rule over all 20-year periods of the test sample, 96% of finishing portfolio balances ended above initial starting level with no portfolio “failures”. The other interesting observation was that in a high majority (82%) of the twenty-year periods required none or only one reduction in the withdrawal rate.

The author goes on to recommend that investors may want to take additional steps to compensate for a period of lower income, derived from reduced withdrawal rates, by building a ‘safe money’ bucket or having access to other sources of ‘backup’ income.

With so many investors on the sidelines over the last few years, incorporating Lynch’s ‘Stay-in-Stocks DGI Strategy’ with a 90% Balance Rule adjustment may be just what conservative investors are looking for if they fear a market correction or crash is just around the corner.