MP Market Review – July 19, 2024

Last updated by BM on July 22, 2024

Summary

This is a weekly installment of our MP Market Review series, which provides updates on the financial markets and Canadian dividend growth companies we monitor on ‘The List’.

- Building Your Dividend Growth Portfolio: How to Invest a Lump Sum in this week’s newsletter.

- Last week, dividend growth of ‘The List’ stayed the course and has increased by +8.8% YTD (income).

- Last week, the price of ‘The List’ was up with a return of +7.9% YTD (capital).

- Last week, there were no dividend announcements from companies on ‘The List’.

- Last week, there were no earnings reports from companies on ‘The List’.

- This week, four companies on ‘The List’ are due to report earnings.

DGI Clipboard

“The best time to plant a tree was 20 years ago. The second best time is now.”

– Chinese Proverb

Building Your Dividend Growth Portfolio: How to Invest a Lump Sum

Ideally, you will have created a Dividend Growth Investing (DGI) business plan that outlines your objectives and how you are going to deploy your hard-earned capital. Next, you will have a list of companies that meet your investment criteria and will select from this list when they are sensibly priced. Finally, you will be patient and build your portfolio over a few years, as not all quality companies will be sensibly priced at the same time.

Our blog follows this process with our model dividend growth portfolio. Paid subscribers can build their portfolios alongside ours, saving time on research and eliminating much of the emotion of investing. We send alerts for every buy or sell action and conduct quarterly performance reviews to track our progress.

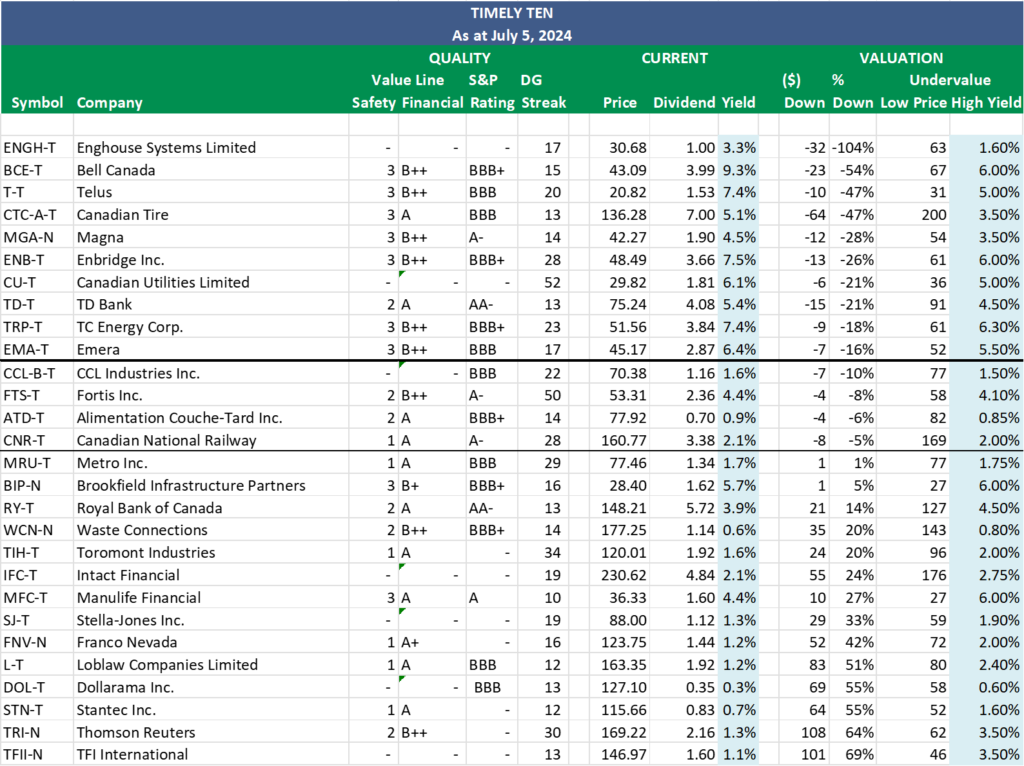

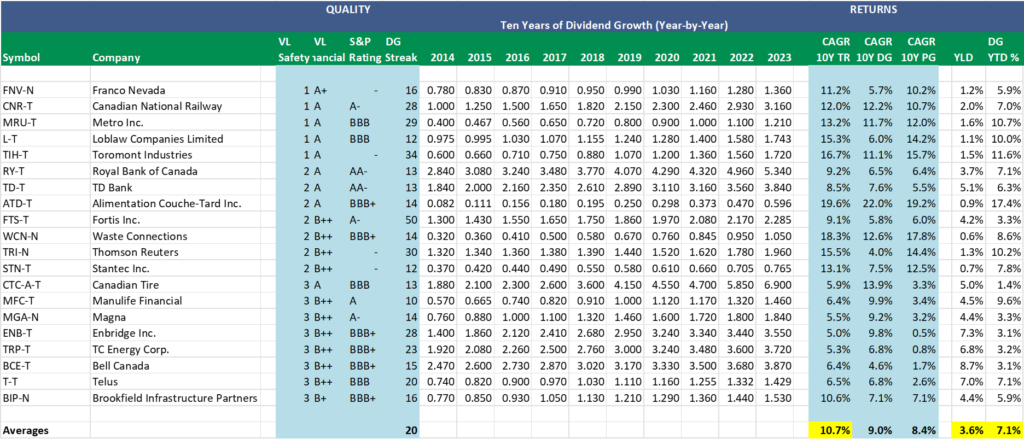

But what if you’re new to the blog, have a lump sum to invest, and want to start quickly? The answer is simple: invest in our All Canadian ‘No-Look’ DGI Portfolio. This portfolio is a streamlined version of ‘The List’ we follow, featuring a diversified selection of the top twenty Canadian stocks, rated for quality by reputable third-party agencies (Value Line and S&P) as of January 2024.

By investing equal amounts in each of these twenty companies, you’re on your way to building a robust DGI portfolio. For more details on how we manage risk and determine when to buy or sell, read the business plan in the premium content section of our site.

All Canadian ‘No-Look’ DGI Portfolio (As of July 19, 2024)

Over time, you can make adjustments to your portfolio, but you now have the foundation of a strong DGI portfolio. Your initial lump sum is already generating a growing income, with a starting yield of 3.6% and dividend growth that has increased by 7.1% year-to-date. By adding to positions when they are sensibly priced and selling overvalued holdings, you can further enhance your total return.

It’s quite remarkable that when you combine the starting yield and dividend growth, it matches exactly with the Compound Annual Growth Rate (CAGR) for the total return of these stocks over the past ten years, leading into 2024 (10.7%).

Remember our magic formula: Yield + Growth +/- Change in P/E = Total Return. The longer your investment horizon, the more predictable your returns become with DGI.

DGI Scorecard

The List (2024)

The Magic Pants 2024 list includes 28 Canadian dividend growth stocks. Here are the criteria to be considered a candidate on ‘The List’:

- Dividend growth streak: 10 years or more.

- Market cap: Minimum one billion dollars.

- Diversification: Limit of five companies per sector, preferably two per industry.

- Cyclicality: Exclude REITs and pure-play energy companies due to high cyclicality.

Based on these criteria, companies are added or removed from ‘The List’ annually on January 1. Prices and dividends are updated weekly.

While ‘The List’ is not a standalone portfolio, it functions admirably as an initial guide for those seeking to broaden their investment portfolio and attain superior returns in the Canadian stock market. Our newsletter provides readers with a comprehensive insight into the implementation and advantages of our Canadian dividend growth investing strategy. This evidence-based, unbiased approach empowers DIY investors to outperform both actively managed dividend funds and passively managed indexes and dividend ETFs over longer-term horizons.

For those interested in something more, please upgrade to a paid subscriber; you get the enhanced weekly newsletter, access to premium content, full privileges on the new Substack website magicpants.substack.com and DGI alerts whenever we make stock transactions in our model portfolio.

Performance of ‘The List’

Last week, dividend growth of ‘The List’ stayed the course and has now increased by +8.8% YTD (income).

Last week, the price return of ‘The List’ was up with a return of +7.9% YTD (capital).

Even though prices may fluctuate, the dependable growth in our income does not. Stay the course. You will be happy you did.

Last week’s best performers on ‘The List’ were TC Energy Corp. (TRP-T), up +6.09%; Metro Inc. (MRU-T), up +4.10%; and Stella-Jones Inc. (SJ-T), up +3.89%.

Enghouse Systems Limited (ENGH-T) was the worst performer last week, down -3.96%.

| SYMBOL | COMPANY | YLD | PRICE | YTD % | DIV | YTD % | STREAK |

|---|---|---|---|---|---|---|---|

| ATD-T | Alimentation Couche-Tard Inc. | 0.9% | $82.05 | 6.9% | $0.70 | 17.4% | 14 |

| BCE-T | Bell Canada | 8.7% | $45.62 | -15.8% | $3.99 | 3.1% | 15 |

| BIP-N | Brookfield Infrastructure Partners | 5.3% | $30.45 | -0.8% | $1.62 | 5.9% | 16 |

| CCL-B-T | CCL Industries Inc. | 1.6% | $73.40 | 26.9% | $1.16 | 9.4% | 22 |

| CNR-T | Canadian National Railway | 2.0% | $165.66 | -0.7% | $3.38 | 7.0% | 28 |

| CTC-A-T | Canadian Tire | 5.0% | $140.29 | 1.2% | $7.00 | 1.4% | 13 |

| CU-T | Canadian Utilities Limited | 5.9% | $30.52 | -5.0% | $1.81 | 0.9% | 52 |

| DOL-T | Dollarama Inc. | 0.3% | $126.95 | 33.6% | $0.35 | 29.5% | 13 |

| EMA-T | Emera | 6.1% | $46.98 | -7.5% | $2.87 | 3.0% | 17 |

| ENB-T | Enbridge Inc. | 7.3% | $50.17 | 3.7% | $3.66 | 3.1% | 28 |

| ENGH-T | Enghouse Systems Limited | 3.3% | $30.35 | -10.7% | $1.00 | 18.3% | 17 |

| FNV-N | Franco Nevada | 1.2% | $124.57 | 13.1% | $1.44 | 5.9% | 16 |

| FTS-T | Fortis Inc. | 4.2% | $55.62 | 1.4% | $2.36 | 3.3% | 50 |

| IFC-T | Intact Financial | 2.0% | $237.83 | 17.0% | $4.84 | 10.0% | 19 |

| L-T | Loblaw Companies Limited | 1.1% | $169.28 | 31.7% | $1.92 | 10.0% | 12 |

| MFC-T | Manulife Financial | 4.5% | $35.62 | 23.3% | $1.60 | 9.6% | 10 |

| MGA-N | Magna | 4.4% | $43.64 | -21.4% | $1.90 | 3.3% | 14 |

| MRU-T | Metro Inc. | 1.6% | $82.50 | 20.4% | $1.34 | 10.7% | 29 |

| RY-T | Royal Bank of Canada | 3.7% | $152.64 | 14.7% | $5.72 | 7.1% | 13 |

| SJ-T | Stella-Jones Inc. | 1.2% | $93.50 | 22.1% | $1.12 | 21.7% | 19 |

| STN-T | Stantec Inc. | 0.7% | $117.18 | 12.0% | $0.83 | 7.8% | 12 |

| T-T | Telus | 7.0% | $21.72 | -8.4% | $1.53 | 7.1% | 20 |

| TD-T | TD Bank | 5.1% | $79.42 | -6.2% | $4.08 | 6.3% | 13 |

| TFII-N | TFI International | 1.0% | $153.61 | 17.1% | $1.60 | 10.3% | 13 |

| TIH-T | Toromont Industries | 1.5% | $125.16 | 11.0% | $1.92 | 11.6% | 34 |

| TRI-N | Thomson Reuters | 1.3% | $162.66 | 13.5% | $2.16 | 10.2% | 30 |

| TRP-T | TC Energy Corp. | 6.8% | $56.41 | 7.8% | $3.84 | 3.2% | 23 |

| WCN-N | Waste Connections | 0.6% | $180.35 | 21.7% | $1.14 | 8.6% | 14 |

| Averages | 3.4% | 7.9% | 8.8% | 21 |

Note: Stocks ending in “-N” declare earnings and dividends in US dollars. To achieve currency consistency between dividends and share price for these stocks, we have shown dividends in US dollars and share price in US dollars (these stocks are listed on a US exchange). The dividends for their Canadian counterparts (-T) would be converted into CDN dollars and would fluctuate with the exchange rate.

Check us out on magicpants.substack.com for more info in this week’s issue….