If you like a safe 5% yield, then companies don’t get much better than CU-T. Their most recent dividend increase put them in an elite class of dividend growers (50-year streak). They are the only Canadian company to achieve such a milestone. The problem with CU-T is that there is very little growth to their dividend so companies with an average starting yield (2.5-3.5%) and high single digit growth, easily catch up within a decade. Be careful when you chase high yielding stocks thinking they will provide you with a growing income in retirement. Of the twenty-seven companies on ‘The List’ only six have a lower yield now, after a decade, than CU-T and all of them had much higher total returns.

Stantec (STN-T)

“In addition to achieving record earnings this year, several important strategic milestones attained in 2021 position us for accelerated value creation in 2022 and beyond,” said Gord Johnston, President and CEO. “The acquisition of Cardno, along with the five other acquisitions we made in 2021, expand our presence in key business lines such as environmental services and the energy transition, and key geographies like the United States and Australia that are poised for strong growth. Looking forward, we see a strong multi-year cycle ahead for the industry which will support expansion of our record 2021 Adjusted EBITDA margin and earnings.”

The company published these highlights:

Q4 2021 Financial Results

- Net revenue, on a constant currency basis, increased 8.7% or $75.0 million, driven by acquisition growth of 6.7% and organic growth of 2.0%; including the effects of foreign exchange, net revenue increased $54.5 million. Without the impact of TMEP, organic growth would have been 4.2%, reflecting strong growth achieved in Canada and Global, and organic growth across most business lines with the exception of Infrastructure which stayed consistent with the prior period.

- Project margin increased 11.3%, or $51.6 million, and increased as a percentage of net revenue from 52.8% to 55.3%, primarily from higher net revenue, a shift in project mix, and strong project execution.

- Adjusted EBITDA from continuing operations increased 2.6% or $3.6 million to $142.1 million, representing 15.5% of net revenue compared with $138.5 million or 16.1% of net revenue in the prior period. The increase in project margin was partly offset by higher administrative and marketing expenses, most notably a $13.4 million increase in share-based compensation expense (146 basis points as a percentage of net revenue) reflecting the revaluation of incentive plans due to an increase in Stantec’s share price. As well, 2020 included the recovery of certain claim costs.

- Net income from continuing operations increased 11.4%, or $1.7 million, to $16.6 million, net income from continuing operations as a percentage of net revenue increased from 1.7% to 1.8%, and diluted EPS increased by 15.4%, or $0.02, to $0.15. Strong project margin, lower non-cash net lease asset and related property and equipment impairments and adjustments for onerous contract costs from the continued execution of the 2023 Real Estate Strategy, and non-cash fair value gains on equity investments contributed to a higher net income, partly offset by lower utilization in the US and higher amortization of intangible assets and acquisition and integration costs related to recent acquisitions.

- Adjusted net income decreased 4.8%, or $3.2 million, to $63.8 million, representing 7.0% of net revenue, and adjusted diluted EPS decreased 5.0%, or $0.03, to $0.57. Q4 2020 adjusted net income benefited from the favorable recovery of claim costs and resolution of certain tax matters.

Full-Year 2021 Financial Highlights

- Full-year net revenue was $3.6 billion, a 2.6% increase on a constant currency basis compared with the prior year, driven by acquisition growth of 3.9%, partly offset by a slight organic retraction. Excluding the impact of the descoped Trans Mountain Expansion Project (“TMEP”), organic growth was 0.3% driven by strong performances in Canada and Global and offset by a slower US recovery. Fluctuations in foreign currencies resulted in negative foreign exchange impacts of 3.9%.

- The Canadian dollar strengthened considerably relative to the US dollar during the year, with the average exchange rate shifting to $1.25 in 2021 from $1.34 in 2020. This reduced 2021 net revenues by $130.7 million. Stantec further estimates that the impact to adjusted EBITDA, adjusted net income, and adjusted diluted EPS was approximately $16.6 million, $6.5 million, and $0.06 per share, respectively.

- Project margin increased $32.8 million or 1.7% to $2.0 billion and increased as a percentage of net revenue from 52.4% to 54.0%, as a result of strong project execution in all geographies and businesses and shifts in project mix.

- Adjusted EBITDA from continuing operations was $573.8 million, approximating amounts generated in 2020 and increasing as a percentage of net revenue by 10 basis points to a record 15.8% from 15.7%. The increase in project margin was partly offset by higher administrative and marketing expenses, most notably a $30.3 million increase in share-based compensation expense (83 basis points as a percentage of net revenue) reflecting the revaluation of incentive plans due to an increase in Stantec’s share price.

- The 2023 Real Estate Strategy contributed more than $0.18 per share in cost savings to net income ($0.15 per share savings to adjusted net income). On a pre-IFRS 16 basis, the cumulative impact from this initiative is estimated to have increased 2021 adjusted EBITDA margin by more than 100 basis points. As further progress was made on the Real Estate Strategy in 2021, additional leased spaces were identified to vacate and sub-let, and expectations for sub-let opportunities were adjusted to reflect current market conditions and outlook. This led to a $24.8 million non-cash net impairment of lease assets and related property and equipment and $12.5 million in onerous contract costs being recorded. Stantec is on track to achieve a 30% reduction in its real estate footprint relative to its 2019 baseline and expects to deliver a further $0.20 to $0.25 contribution to earnings per share by the end of 2023.

- Net income from continuing operations increased 26.1%, or $41.6 million, to $200.7 million; net income margin from continuing operations increased 1.2% from 4.3% to 5.5%, and diluted EPS increased 26.8%, or $0.38, to $1.80. Factors contributing to higher net income include project margin growth, lower interest and depreciation, unrealized fair value gains from equity investments, the combined effects of the 2023 Real Estate Strategy, and a lower effective tax rate partially offset by increased acquisition and integration costs.

- Adjusted net income from continuing operations increased 8.4%, or $21.0 million, to $269.9 million, representing 7.4% of net revenue, an improvement of 60 basis points, and adjusted diluted EPS increased 9.0%, or $0.20, to $2.42.

- Contract backlog stands at a record $5.1 billion—a 17.3% increase from December 31, 2020—representing approximately 13 months of work (11 months of work in 2020). Year over year, backlog grew 11.9% through acquisitions and 6.7% organically, with organic growth in all geographies. Of particular note, US backlog achieved 10.2% organic growth, with US Environmental Services recording over 50% organic growth. Further, Environmental Services backlog across all Stantec stands at over $1 billion, a new high-water mark for this business operating unit.

- Net debt to adjusted EBITDA was 1.8x at December 31, 2021 —within the guideline range of 1.0x to 2.0x. The ratio increased as a result of additions to net debt from acquisitions made in the fourth quarter.

- Operating cash flows from continuing operations decreased 34.1% from $602.6 million to $397.0 million; this was mainly due to decreased cash receipts from clients, negative foreign exchange impacts, and increased payments paid to suppliers.

- Days sales outstanding (“DSO”) was 75 days at December 31, 2021 and 2020, well below the expectation of 80 days.

- In 2021, 939,482 common shares were repurchased for an aggregated price of $50.7 million under the normal course issuer bid which was renewed on November 9, 2021, to allow for the repurchase of up to an additional 5,559,312 common shares.

- On February 23, 2022, Stantec’s Board of Directors declared a dividend of $0.18 per share, payable on April 18, 2022, to shareholders of record on March 31, 2022, representing an 9.1% increase on an annual basis.

Outlook

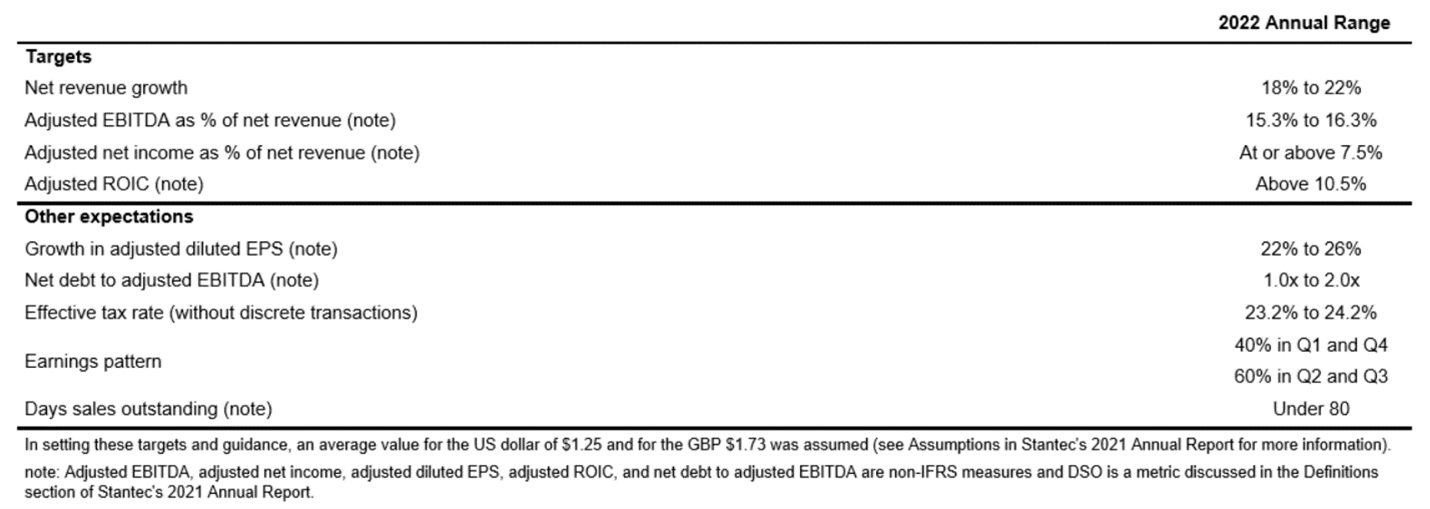

Targets for 2022 are based on the assumption of a continued gradual global recovery but may not be valid should any of our key geographies experience a severe worsening of the pandemic.

Net revenue is expected to increase 18% to 22% in 2022, and organic net revenue growth is expected to be in the mid to high single digits, weighted to the second half of the year. Organic growth in the US is expected to be in the high single digits, driven by growing momentum as evidenced by Stantec’s record-high US backlog and project opportunities arising from the $1.2 trillion infrastructure stimulus bill. After a year of robust organic growth in Canada in 2021, high levels of activity are expected to be maintained, driving 2022 organic growth in the low single digits. Organic growth in Global is expected to achieve high single to low double-digit growth propelled by strong economic growth, continued demand, and stimulus in infrastructure sectors.

Project margin as a percent of net revenues is expected to be relatively consistent in 2022 compared to 2021. Adjusted EBITDA margin is anticipated to be in the range of 15.3% to 16.3%, reflecting investments in internal resources to support growth and the commercialization of new innovations and technologies, and increased discretionary spending (albeit not to pre-pandemic levels). Adjusted EBITDA margin in Q1 2022 will likely be at or below the low end of this range because of the additional effects of regular seasonal factors in the northern hemisphere and the protracted ramp-up of US activities and major projects awarded in Q4 2021. The higher end of the range is expected to be reached by the second half of 2022 driven by high organic net revenue growth and increased utilization in the US operations.

Adjusted net income is expected to continue to benefit from the 2023 Real Estate Strategy, which remains on track to achieve a 30% reduction in real-estate footprint compared with a 2019 baseline and a cumulative $0.35 to $0.40 per share by the end of 2023. With $0.15 recognized in 2021, the remaining $0.20 to $0.25 per share is expected to be generated approximately evenly between 2022 and 2023. For 2022, this, in conjunction with continued benefits from tax planning strategies, is expected to drive an adjusted net income margin of 7.5% or greater as a percent of net revenue. As a result, adjusted diluted EPS is expected to grow 22% to 26% in comparison to 2021.

CCL Industries seems to have been impacted by the effects of inflation with their earnings up a bit but not at the rate as in prior years. The recent dividend increase of 14.3% is not something to ignore as it shows a lot of confidence by management in the operations outlook of the business (the safest dividend is the one just hiked). Share price weakness in 2022 has brought this 20-year dividend grower closer to the ‘sensible price’ range we look for.

Royal Bank (RY-T)

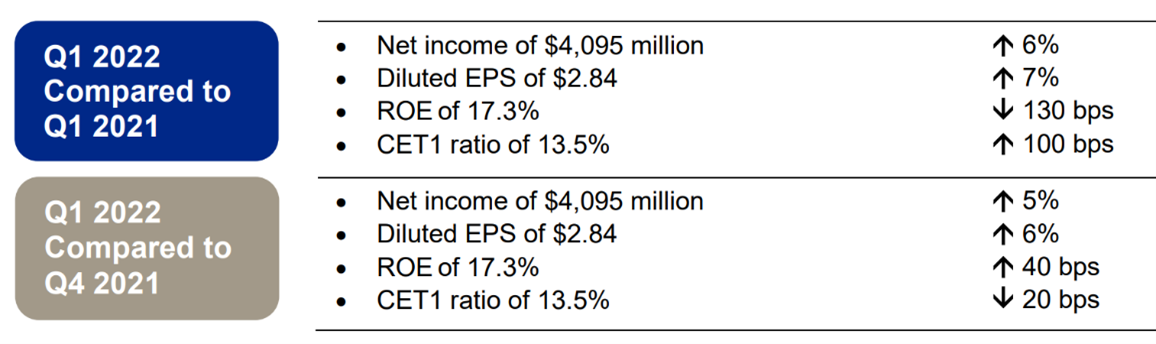

“RBC’s firstquarter performance reflects the significant momentum we continue to build while facing change and uncertainty in the current operating environment. This is a testament to our scale, diversified business model, and strategic investments in technology, talent and innovation to create differentiated value for our clients and shareholders. While the Omicron variant has created headwinds to the global economic recovery over the past quarter, RBC employees remained unwavering in their commitment to supporting our clients and communities. I’m proud of how they continue to make a difference in the lives of those we serve. Looking forward, we remain focused on our Purpose-led approach to delivering the advice, products and services our clients need in a changing world, while also accelerating our commitments to enable a sustainable and inclusive future.” Dave McKay, RBC President and CEO

The company published these highlights:

Q1 2022 Financial Results